Have they met with you to discuss how recent market fluctuations could

affect your financial plans? When was the last time the two of you sat down to

really discuss goals?

It’s imperative to re-visit financial plans often to make sure they’re

in line with changes in the market, your life, your financial situation and/or

your goals. If you feel your current plan may be out of date, you’re not alone.

Maybe it’s

time for a change.

I work with a select group of clients with whom I have built trusted

personal relationships. My commitment to their financial well-being is strong.

They know I’ll be there when they have questions or concerns. They know I’m

available, knowledgeable, and proactive.

In today’s economy, a good financial professional should do more than merely “check-up” on a client every now and then. You need someone who will actively follow your investments, someone who listens when you tell your story, someone who provides leadership at the right time.

If you feel your portfolio could use a little more care and attention … please contact me. I can be reached at (215) 766-7002 or via email at bchavez@aeinvestmentsgroup.com.

See if you are prepared to begin your retirement by answering four key questions.

How do you know you are psychologically ready to retire? As a start, ask yourself four questions.

One, is your work meaningful? If it is emotionally and psychologically fulfilling, if

it gives you a strong sense of purpose and identity, there may be a voice

inside your head telling you not to retire yet. You may want to listen to it.

It can be tempting to see retirement as a “finish line”: no more

long workdays, long commutes, or stressful deadlines. But it is really a

starting line: the start of a new phase of life. Ideally, you cross the “finish

line” knowing what comes next, what will be important to you in the future.

Two, do you value work or leisure more at this point in

your life? If the answer is

leisure, score one for retirement. If the answer is work, maybe you need a new

job or a new way of working rather than an exit from your company or your

profession.

An old saying says that retirement feels like “six Saturdays and a

Sunday.” Fantastic, right? It is, as long you don’t miss Monday through Friday.

Some people really enjoy their careers; you may be one of them.

Three, where do your friends come from? If very little of your social life involves the people

you work with, then score another point for retirement. If your friends are

mainly your coworkers, those friendships may be tested if you retire (and you

may want to try to broaden your social circle for the future).

At a glance, it might seem that an enjoyable retirement requires

just two things: sufficient income and sufficient return on your investments.

These factors certainly promote a nice retirement, but there are also other

important factors: your physical health, your mental health, your relationships

with family and friends, your travels and adventures, and your outlets to

express your creativity. Building a life away from work is a plus.

Four, what do you think your retirement will be like? If you think it will be spectacularly different from your

current life, ask yourself if your expectations are realistic. If after further

consideration they seem unrealistic, you may want to keep working for a while

until you are in a better financial position to try and realize them or until

your expectations shift.

Ideally, you retire when you are financially, emotionally,

and psychologically ready. The era of the

“organization man” retiring with a gold watch and a party at 65 is gone; the

cultural forces that encouraged people to stop working at a certain age aren’t

as strong as they once were.

Why you are retiring is as important as when you choose to retire. When you are motivated to retire, you see retirement as a beginning rather than an end.

Are you prepared for retirement? Will you have enough to retire? Get your retirement plan in place. Schedule a FREE no-obligation initial consultation with us today:

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Hello everyone. Brent Chavez, Aequitas Equitas Investment Group. I hope this video finds you well. It is Thursday afternoon, and we are in the midst of a market crash that is somewhat unprecedented in it being a draw down in such a short period of time. I just wanted to give you a follow up and tell you again, where we stand, a follow-up to the two videos I sent you this last month of what we’re doing to protect your portfolios, has been working tremendously. But, I want to go a little bit deeper as to what we saw, what we’re seeing that made us do something that is very rare for us as a practice to go so defensive. As many of you know, it’s not something we like to do, those that have been with us for a long period of time.

I’m going to share with you some things that we saw going on at the end of January that concerned us. As I mentioned in my video from January, we had had a big run up. We had stretch valuations in the markets. We were seeing a flight to bonds, globally, inflows to bonds were really up ticking. And as the yields were dropping, buyers would come in, grab those bonds. No matter how low those yields were, buyers were showing up. And at the same time seeing the deterioration of the many individual stocks in indexes in sectors globally that was a concern to us. We’re going to touch on again this is not going to be all encompassing of what we’re looking at for you on a daily, weekly, monthly basis, but just a little bit deeper than the last two videos have been.

So again, back here in January, the S&P had hit a short term target that we had around 3300. We had noticed as we looked around, there were some canaries in the mines and red flags, so to speak. We’re going to take a look at them.

We see here some sideways action in the S&P 500. We saw it ticking up for a few weeks after we went defensive with all your portfolios, but we felt that that was more or less a “sucker’s rally,” as I like to call people being taken in before the fall off the cliff, potentially was going to take place. We’re here today as we do this video around 3000, a little over 3000. So again, a pretty sizable pullback in a very short period of time, not something that we knew was going to happen, not something that we said was absolutely going to happen… we actually said we don’t know what tomorrow brings when it comes to the stock markets. The only thing we can do and we do do for all of you is to look at the data and make educated decisions based on the data that we see come in.

We’re going to move a little bit further into our next chart.

Here was something that got concerning here over a couple month period – this is the chart of the 10 year Treasury. We saw yields collapsing in that 10-year. It touched against 1.39 for the 10-year Treasury. But the problem was, buyers kept showing up, flows kept going that way, it was a little bit of what we thought to be a warning sign. In fact, a very important chart to look at as to why we want to be more neutral and defensive in our portfolios. It has collapsed through this resistance and I feel moving forward we’re going to see much lower yields, much lower interest rates, Federal Reserve it’s important for you to come into lower rates. We’re getting less and less ammo… as you see the scale, we’re getting to the fractions because there’s not much to zero from here. So again we’re concerned, though, that it may push lower for the foreseeable future. So we want to stay positioned as we are for now.

The next chart that we’re looking at is the financials.

I talk about being able to have confirmation besides the S&P and the Dow Jones. Looking at the charts we want to see some other charts that really give us confirmation that these moves are real, that there’s more than just a handful of stocks like the S&P 500 – basically you have 5 stocks pulling it up the last several weeks, the big mega cap stocks, where the rest of the stocks in that index were breaking down, deteriorating from a technical standpoint. Financials is an important part to any stock market rally that is sustainable or able to move forward. In the past I had talked about this resistance, all time highs in the XLF ETF representing financials in the S&P 500. All time high back in 2008, we hit it in ‘16, pull down before the next several years sideways, and than finally joined the rally of the S&P 500. But, again hit that resistance and the S&P 500 continued to move up and financials moved sideways… no confirmation that this rally had legs to move much higher.

We’re going to see that on a chart here.

Here’s where we see confirmation of the S&P, in purple, XLF moving, confirming these moves up. We started seeing issues and real big issues here (past few weeks), a canary in the mine.

Let’s look at our next chart and data we’re looking at.

The Dow Jones Industrial one of the indexes that every night you see or hear in the news, “record high” with the S&P 500, the NASDAQ. When the Dow Jones Industrial is making moves we want some confirmation that it is a real sustainable move. And we want to get that confirmation from the Dow Jones Transports, DJT. What is the difference?

Well, here’s the light blue line, this is the Dow Jones Industrial, again you see that on TV every night, the dark blue line is the Dow Jones Transports. So the Dow Jones Industrial, 30 industrial companies, making a lot of goods that Americans consume and the globe consumes. So with that being said, the companies that move the goods throughout the country throughout the world should be doing similarly good. And we saw something that happened, starting back at the end of last year, we started to see a separation of those charts. We started to see that we were not getting confirmation. When I sent out the video back in January, the Dow Jones Industrial had done about 13% in the last year and the Dow Jones Transports had done 3%.

So again we were seeing a divergence that was growing and growing – red flag or a canary in the mine. Again, a big divergence was taking place here in January, a sign that not all was well for the markets to continue much higher and uninterrupted with some form of a pullback.

Let’s look at our next piece of data we were looking at. Oil.

Because what happened was the markets were humming along, hitting all time highs, but oil was falling off the cliff, about $10 a barrel, in that very short period of time of about a month. If the economy’s rocking and rolling, the global economy is ready to take off and help support the S&P 500 and Dow Jones companies to really help their evaluations from a fundamental standpoint and help them grow into 2020, 2021… but, oil was telling a different story. Again, it was another thing that had us concerned that we might want to be more defensive in our posture.

Here’s another chart that we want to take a look at.

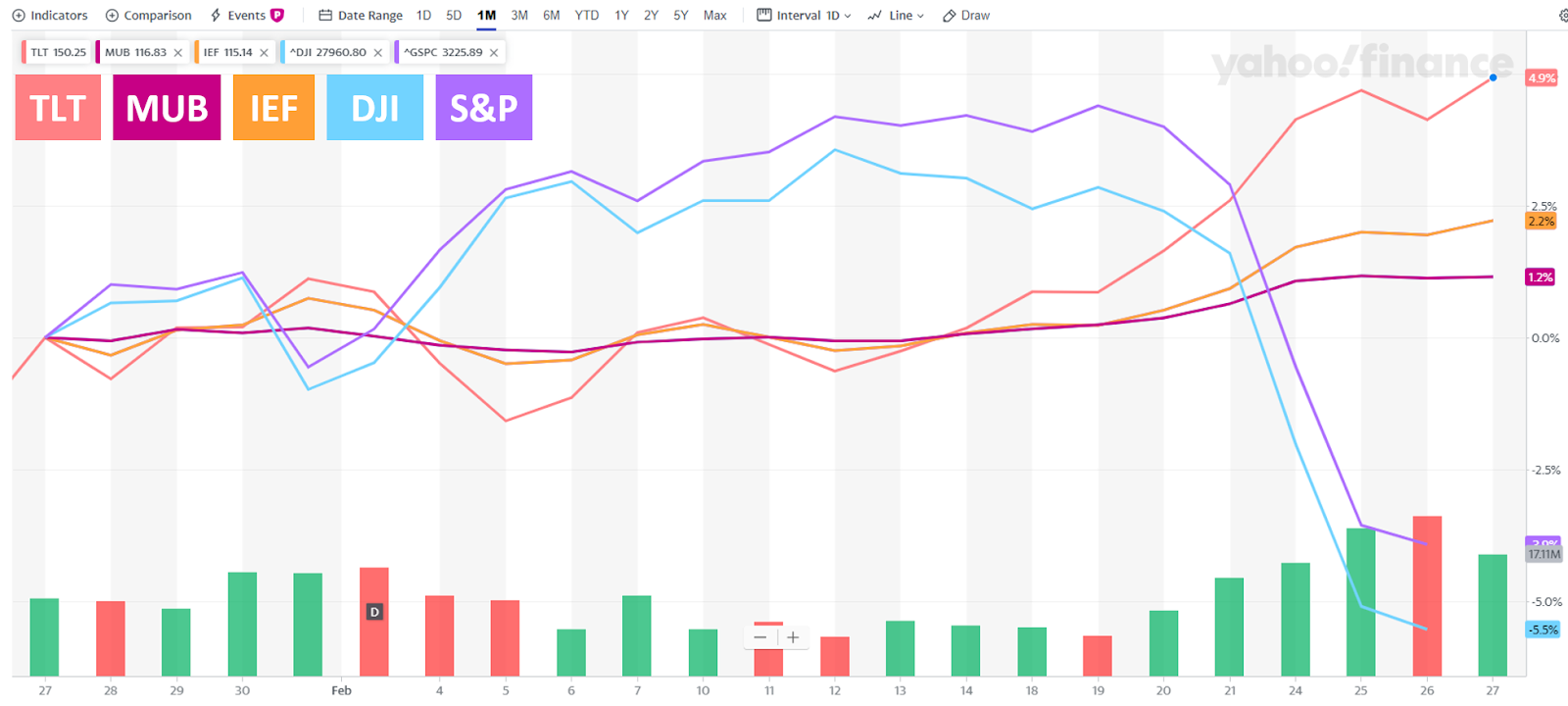

So, back to the positions we moved to, very defensive – treasuries, municipal bonds, 10 and 20-year treasuries, and utilities – all very defensive in nature in our portfolio build. Here’s why. Inflows represented by these three here, treasuries, municipal bonds, 10 and 20-year Treasury. We saw inflows starting back here (end of January, beginning of February) into bonds, very high. We had this continuation of a rally again that had no support, no confirmation from any of the other sectors that the yields from the treasuries on the 10, 20 or 30-year, were crashing. And ultimately, here’s what has happened. Look at those treasuries and municipal bond positions up and then your S&P 500 and Dow Jones down this past week.

So again, it was the correct move to make it that time. And again, this is just part of what we’re looking at. We also look at credit spreads and many other things that most of you would probably find boring – basically, you’d probably rather go to the dentist and have your teeth cleaned then hear about all of those other things. But this is what we eat, this is what we breathe, this is what we love to do.

I want to thank all of you for allowing me to be part of your life. If you have any questions, any concerns about what we’ve discussed and what you’re hearing, please feel free to give me a call. Because at this point, as I mentioned in the other videos, the Coronavirus was that outlier, the icing on the cake. All this data that we were looking at, that was really the thing that said hey, I don’t think it’s being factored in. I don’t think China is telling us the whole story. We don’t know where that’s going to play out at this point and that’s far from over and we don’t know how that is going to affect our projections moving forward. But, time will tell.

So, in the meantime, we will be defensive. We will be here to answer any questions – give us a call, and have a wonderful sunny Thursday afternoon.

*Charts are from Yahoo! Finance and JC Parets

The information contained herein has been derived from sources believed to be reliable, but is not guaranteed as to accuracy and does not purport to be a complete analysis of any security, company, industry, or index. This report is not to be construed as an offer to sell or a solicitation of an offer to buy or sell any security. It is not intended to provide advice tailored to your specific situation. Past performance is no guarantee of future success. The information in this report in no way attempts to provide accounting, legal or tax advice. Investment advisory services offered through Motiv8 Investments, an SEC Registered Investment Advisor.

Much is out there about the classic financial mistakes that plague

start-ups, family businesses, corporations, and charities. Aside from these

blunders, some classic financial missteps plague retirees.

Calling them “mistakes” may be a bit harsh, as not all of them

represent errors in judgment. Yet whether they result from ignorance or fate,

we need to be aware of them as we plan for and enter retirement.

1. Leaving work too early. As Social Security benefits rise about 8% for every year you delay receiving them, waiting a few years to apply for benefits can position you for higher retirement income. Filing for your monthly benefits before you reach Social Security’s Full Retirement Age (FRA) can mean comparatively smaller monthly payments. Meanwhile, if you can delay claiming Social Security, that positions you for more significant monthly benefits.1

2. Underestimating medical bills. In its latest estimate of retiree health care costs, the Center for Retirement Research at Boston College says that the average retiree will need at least $4,300 per year to pay for future health care costs. Medicare will not pay for everything. That $4,300 represents out-of-pocket costs, which includes dental, vision, and long-term care.2

3. Taking the potential for longevity too lightly. Actuaries at the Social Security Administration project that around a third of today’s 65-year-olds will live to age 90, with about one in seven living 95 years or longer. The prospect of a 20- or 30-year retirement is not unreasonable, yet there is still a lingering cultural assumption that our retirements might duplicate the relatively brief ones of our parents.3

4. Withdrawing too much each year. You may have heard of the “4% rule,” a guideline stating that you should take out only about 4% of your retirement savings annually. Many cautious retirees try to abide by it.

So, why do others withdraw 7% or 8% a year? In the first phase of retirement, people tend to live it up; more free time naturally promotes new ventures and adventures and an inclination to live a bit more lavishly.

5. Ignoring tax efficiency & fees. It can be a good idea to have both taxable and tax-advantaged accounts in retirement. Assuming your retirement will be long, you may want to assign this or that investment to its “preferred domain.” What does that mean? It means the taxable or tax-advantaged account that may be most appropriate for it as you pursue a better after-tax return for the whole portfolio.

Many younger investors chase the return. Some retirees, however, find a shortfall when they try to live on portfolio income. In response, they move money into stocks offering significant dividends or high-yield bonds – something you might regret in the long run. Taking retirement income off both the principal and interest of a portfolio may give you a way to reduce ordinary income and income taxes.

6. Avoiding market risk. Equity investment does invite risk, but the reward may be worth it. In contrast, many fixed-rate investments offer comparatively small yields these days.

7. Retiring with heavier debts. It is hard to preserve (or accumulate) wealth when you are handing portions of it to creditors.

8. Putting college costs before retirement costs. There is no “financial aid” program for retirement. There are no “retirement loans.” Your children have their whole financial lives ahead of them. Try to refrain from touching your home equity or your IRA to pay for their education expenses.

9. Retiring with no plan or investment strategy. An unplanned retirement may bring terrible financial surprises; the absence of a strategy can leave people prone to market timing and day trading.

These are some of the classic retirement planning mistakes. Why not plan to avoid them? Take a little time to review and refine your retirement strategy in the company of the financial professional you know and trust.

Do you have your retirement plan in place? Set up your FREE initial consultation with Brent E Chavez today:

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The I.R.S. increased the annual contribution limits on IRAs, 401(k)s, and other widely used retirement plan accounts for 2020. Here’s a quick look at the changes.

• You can put up to $6,000 in any type of IRA. The limit is $7,000 if you will be 50 or older at any time in 2020.1,2

• Annual contribution limits for 401(k)s, 403(b)s, the federal Thrift Savings Plan, and most 457 plans also get a $500 boost for 2020. The new annual limit on contributions is $19,500. If you are 50 or older at any time in 2020, your yearly contribution limit for one of these accounts is $26,000.1,2

• Are you self-employed, or do you own a small business? You may have a solo 401(k) or a SEP IRA, which allows you to make both an employer and employee contribution. The ceiling on total solo 401(k) and SEP IRA contributions rises $1,000 in 2020, reaching $57,000.3

• If you have a SIMPLE retirement account, next year’s contribution limit is $13,500, up $500 from the 2019 level. If you are 50 or older in 2020, your annual SIMPLE plan contribution cap is $16,500.3

• Yearly contribution limits have also been set a bit higher for Health Savings Accounts (which may be used to save for retirement medical expenses). The 2020 limits: $3,550 for individuals with single medical coverage and $7,100 for those covered under qualifying family plans. If you are 55 or older next year, those respective limits are $1,000 higher.4

Have questions? Please contact us at (215) 766-7002 or info@aeinvestmentsgroup.com.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.